Tax Topics

These are the topics about which departments most frequently ask. If what you need isn't included, contact us at [email protected].

Tax Tips

- Tax Tip: Account Codes for Student Payments - July 2024

- Tax Tip: Payments to Non-US Taxpayers - June 2024

- Tax Tip: Retail Delivery Fee (RDF) - May 2024

- Tax Tip: Discounts - April 2024

- Tax Tip: Sales Tax Rate Increases - March 2024

- Tax Tip: Payments to Non-Student Individuals - February 2024

- Tax Tip: Tax forms, where to send, where to get assistance - January 2024

- Tax Tip: “B” Visa / Visa Waiver Payments - December 2023

- Tax Tip: Determining Whether Support is a Scholarship - November 2023

- Tax Tip: Sales Tax Sourcing - October 2023

- Tax Tip: Payments to Students, updated - September 2023

- Tax Tip: Regents Tuition Benefit Program - August 2023

- Tax Tip: Increasing Metro Area Sales Tax Rates - July 2023

- Tax Tip: Scholarship Support to Foreign Visitors - June 2023

- Tax Tip: External Sales and Sales Tax - May 2023

- Tax Tip: Employee Gift Card Reporting - April 2023

- Tax Tip: Resources for personal taxes - March 2023

- Tax Tip: PCard Purchases and Sales Tax - February 2023

- Tax Tip: 1099s Sent to the University - January 2023

- Tax Tip: Sales Tax on Disposal of Computers - December 2022

- Tax Tip: Employee Gifts - November 2022

- Tax Tip: Tax Management Office Info - October 2022

- Tax Tip: Regents Scholarship (Regents Tuition Benefit Program) Income Tax Exclusion - September 2022

- Tax Tip: Sales Tax on Purchases - March 2021

- Tax Tip: Faculty Speaking Engagements and Directing the Proceeds to the University - October 2020

Minnesota Sales Tax (Sales Tax When Selling, Sales Tax When Purchasing)

Most purchases made by the University are exempt from sales tax. However, taxable property and taxable services sold by the University are subject to sales tax (unless the purchaser is exempt from sales tax, or an item is shipped out of Minnesota). Like any other business, we must charge sales tax on sales, so we need to be aware of what items are taxable and the appropriate tax rate that applies to the sales.

Sales Tax When Selling

If your department makes sales (frequent or occasional, including "one time" transactions to dispose of old equipment) you should consult the administrative policy Selling Goods and Services to External Customers and the related procedure Tax Considerations Pertaining To External Sales Transactions.

- Job Aid - Sourcing Transactions for Sales Tax - October 2023

- State and Local Sales Tax Rates On University of Minnesota System Campuses effective Apr 1, 2024

- State and Local Sales Tax Rates On University of Minnesota System Campuses Oct 1, 2023 through March 31, 2024

- State and Local Sales Tax Rates On University of Minnesota System Campuses Oct 1, 2019 through Sept 30, 2023

- Selling Events, for example: Farmer's Market, Craft Fair

Minnesota laws impose a sales tax rate based on the destination of the sale. If a buyer picks up an item at the seller’s location, the rate at the seller’s location applies. If the goods are shipped to another location in Minnesota, the rate at the “shipped to” address applies. If the items are shipped out of Minnesota, Minnesota sales tax does not apply.

The Minnesota Department of Revenue provides information on local tax rates in Fact Sheet 164, entitled Local Sales and Use Taxes. Contact the University Tax Management Office at [email protected] if you need assistance in determining the appropriate tax rate to charge.

Sales Tax When Purchasing

The University of Minnesota is exempt from state and local sales taxes on many of its purchases in Minnesota. This exempt status does not apply when purchasing any of the following:

- Lodging

- Prepared food

- Candy

- Soft drinks

- Motor vehicles

- Waste disposal services

- Alcohol

- Airfare

The above exclusions from the University's exempt status are listed on the Form ST3, Certificate of Exemption. Tax should be paid when charged by the seller on these items.

Although a University buyer needs to understand when the University’s exempt status does not apply, the definitions of prepared food, candy, and soft drinks are extremely complicated. It is reasonable for employees to rely on food sellers to know whether the specific items they are selling are taxable or not. As long as the University buyer does not represent to the seller that the University is exempt on the food items, the seller will charge tax when applicable.

One approach when buying food items is to separate food items from nonfood items and inform the seller that we are not exempt on any of the food purchases. You may want to make two charges on your PCard, one for nonfood items on which the seller should not charge tax, and one for the food items, some of which will likely be subject to sales tax as determined by the seller.

- Procedure: Making University Tax Exempt Purchases

Additional Tax Information

Tax Management Office Guideline

National Sales Tax (Purchasing in Other States)

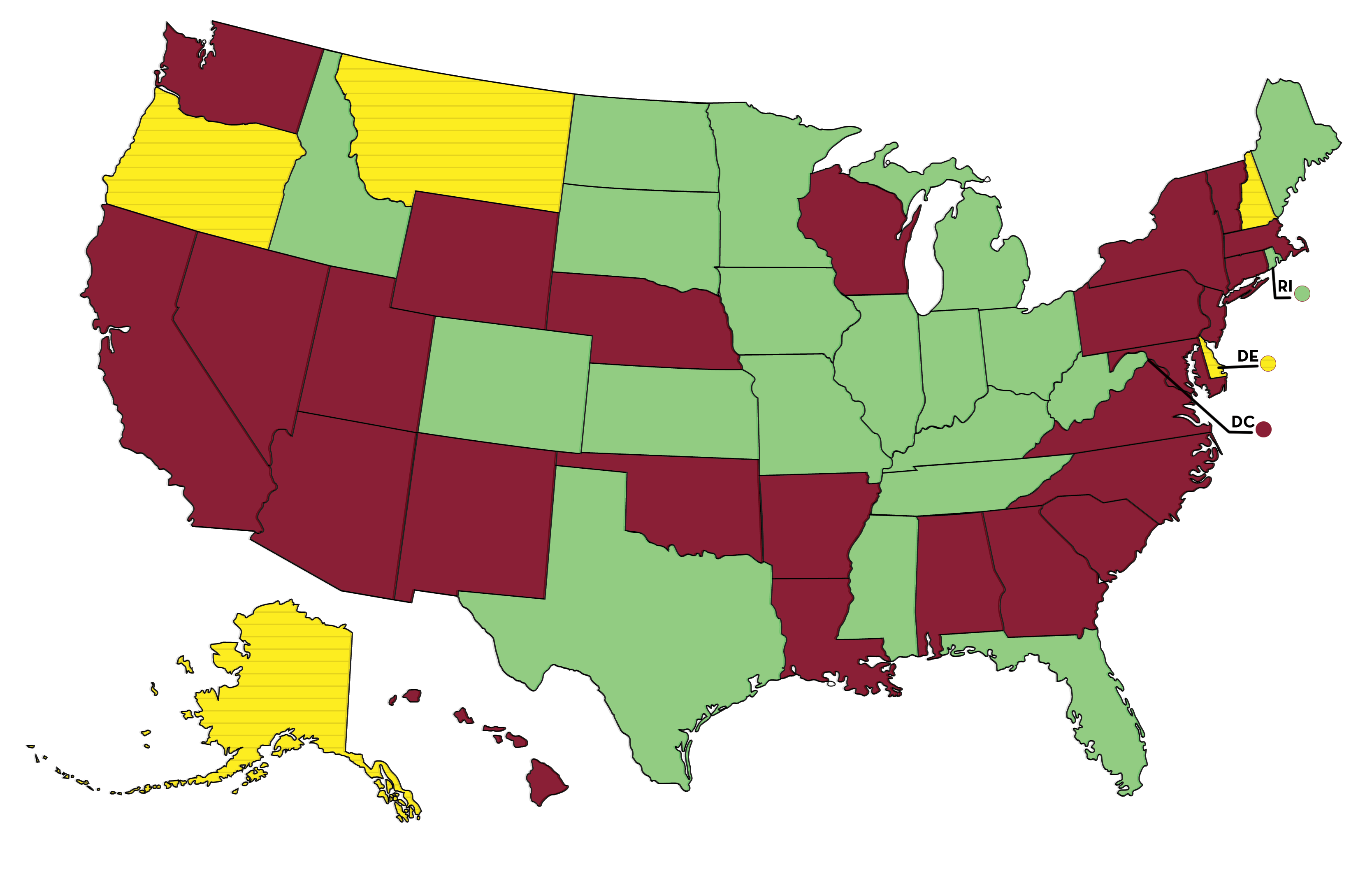

The University of Minnesota is exempt from sales tax on certain purchases within the states shown in light green on the map of the United States below (also listed in text below, under the heading "States with exemption agreements"). These exemptions apply only to goods and/or services purchased within those states directly with University funds, that is, purchased with a University issued PCard, University issued Travel Card, or University issued checks. Strict penalties can be enforced for misusing or misrepresenting exempt status.

The scope of exemption within each state varies. There is a list below titled "States with exemption agreements" that provides more information. Click on the state name for more information on the University's tax status within that state. When traveling to other states and making University purchases, or if University purchases are being shipped by the seller to an address out of Minnesota, check to see if your purchase can be made exempt from tax in that state. Follow the instructions provided in the state link to determine next steps.

Because sales are "sourced" to the destination state, items shipped to Minnesota from vendors located in other states are considered Minnesota sales. Use the Minnesota ST3 to purchase these items exempt.

States with no sales tax

- Alaska

- Delaware

- Montana

- New Hampshire

- Oregon

States and District of Columbia without an exemption

- Alabama

- Arizona

- Arkansas

- California

- Connecticut

- District of Columbia

- Georgia

- Hawaii

- Louisiana

- Maryland

- Massachusetts

- Nebraska

- Nevada

- New Jersey

- New Mexico

- New York

- North Carolina

- Oklahoma

- Pennsylvania

- South Carolina

- Utah

- Vermont

- Virginia

- Washington State

- Wisconsin

- Wyoming

Inflation Reduction Act (IRA) Energy Tax Credits

The Inflation Reduction Act (IRA) is a federal law that was passed in August 2022. It includes new tax credits and substantial changes to existing credits and deductions. These changes were broadly intended to incentivize adoption of clean energy technology, and job creation.

The Tax Management Office has developed some short summaries of provisions that we anticipate may be most relevant for the University. These summaries are for University community use only and should not be used to provide tax advice.

Please be aware that guidance from the IRS is ongoing. These guides will be updated over time as needed. If you have questions about possible projects and whether credits could apply, contact TMO at [email protected].

Guides for Key Concepts

Guides for Specific Credits

International Tax

Operations in countries outside of the United States may create tax liabilities for the University while conducting activities in those countries and for University employees and/or University contractors performing services in those countries. A determination of the liabilities relating to each country can only be done on a case by case basis. The Tax Management Office utilizes the services of the Program and Strategy Alliance of the University to address these issues.

Through Global Operations, the Tax Management Office works with the units across campus to assure comprehensive and timely response to international operations questions in the areas of tax, banking and cash management, purchasing, legal, human resources, and compliance. For further information, contact Kevin Dostal Dauer, the Director of Health, Safety, and Compliance.

The University of Minnesota does not have a VAT (Value Added Tax) Number. For information about the VAT Number, go to the Tax Management Office Guideline TMOG #6.

Tax Management Office Guideline

Charitable Contributions (Gifts)

The University Board of Regents has designated the University of Minnesota Foundation (UMF) as the central development office of the University. While the University will accept gifts made directly to the University, absent unique circumstances making a direct gift to the University more appropriate, donors shall be requested to make gifts to one of the recognized foundations. The University of Minnesota Foundation (UMF) has the responsibility to see that all gifts are receipted and recorded in accordance with federal tax law. (See University Board of Regents Policy Gift Solicitation and Acceptance.)

UMF development office: give.umn.edu

When the IRS determined the University’s exempt status as that of an integral part of the state of Minnesota, it provided the following guidance with respect to contributions given to the University:

Because we have determined that the University of Minnesota is an integral part of the State of Minnesota for federal tax purposes, contributions to or for the use of the University are contributions to or for the use of a state. Accordingly, contributions to or for the use of the University are contributions to or for the use of an entity described in section 170(c)(1) of the Internal Revenue Code of 1986, as amended, and are for exclusively public purposes and are therefore generally deductible under section 170(a)(1) as contributions to a “governmental unit” described in section 170(b)(1)(A)(v). Furthermore, bequests and gifts made to the University are deductible for federal estate and gift tax purposes under section 2055(a)(1) and section 2522(a)(1), respectively.

As an integral part of the state, the University is not a private foundation for the purposes of either the income tax deduction limitations on charitable contributions by taxpayers or the taxable expenditure rules for grants made by private foundations. See code §170(b)(1)(A)(v); Treas. Reg. § 53.4945-5(a)(4)(ii).

Tax Management Office Guideline

Job Aids

- Job aid for processing Form 8283

Employment Related Taxes

Following are convenient links regarding tax issues and procedures that may be of interest to University of Minnesota staff and faculty. The Tax Management Office is a consulting group that supports U departments with business tax needs. We are not able to help individuals with individual tax questions.

Office of Human Resources

The University of Minnesota Office of Human Resources provides payroll information about compensation and taxes for University employees both on their website and within MyU on the My Pay tab.

Accountable Plan

The University of Minnesota has an accountable plan for employee reimbursements. An accountable plan is where reimbursements and/or other expense allowance arrangements must meet certain IRS requirements related to business-connection and substantiation, and requires that amounts in excess of substantiated expenses be returned in a timely manner. Amounts paid under an accountable plan are excluded from the individual's income. Reimbursements made that do not meet the requirements of the accountable plan are taxable. A statement regarding your employer's accountable plan is available, should the IRS ask you for such a statement.

Employee Recognition Awards

What are the tax implications of providing and receiving employee recognition awards? The links below provide guidance on the taxability of various items, including cash, gift cards, and tangible personal property. If taxable awards are made to employees, the awarding department should contact Payroll for proper reporting procedures.

University Employee Recognition Awards

Employee Retirement Savings Plans

The University of Minnesota contributes to a variety of retirement plans that provide benefits for the various employee groups (including faculty) at the University. The University Tax Management Office works with the Office of Human Resources - Employee Benefits, to ensure that the University is complying with federal tax requirements relating to retirement plans. For information on your retirement accounts, visit the Office of Human Resources' page on retirement savings plans.

Taxation of Relocation Expenses

Effective January 1, 2018, relocation expenses are subject to income tax. See the Relocating Employees policy for information about taxable relocation allowances.

Additional Contacts

Employees or former employees with questions regarding W-2s or 1099-Rs should call the Office of Human Resources Call Center at 612-624-8647 or email [email protected].

Employees or former employees with questions on benefits should call Employee Benefits at 612-624-8647 or 800-756-2363, or email [email protected].

Individuals with questions on 1099-MISC should call the Financial Helpline at 612-624-1617 or contact the Controller's Office at [email protected].

See the Office of Human Resources Pay and Taxes page for W-2 and W-4 information.

Forms 1099, W-2, 1042-S, 1098-T and Other Reporting

If a University department receives a 1099 form from outside of the University, including 1099-C, 1099-DIV, 1099-INT, 1099-G, 1099-K, 1099-MISC, 1099-NEC, or 1099-PATR, please either send it via campus mail to the address below or email it to [email protected]:

Tax Management Office

University Office Plaza, Suite 100

Campus Mail Code 2715

We accept all 1099s for the University as the forms may be used in the U's annual tax filing. If you email them to us, you may keep the originals for your records or recycle them.

Tax Forms Not Handled by the Tax Management Office

These forms are handled by the departments most closely associated with their content. In accordance with IRS guidelines, these forms are mailed on or before January 31st of each year.

- W-2 Forms and 1042-S Forms: If you have questions regarding your W-2 or 1042-S, please consult the Human Resources Payroll Department at 612-624-8647 or [email protected]. For duplicate W-2 Forms, login to MyU, click on My Pay, then select "W-2 Reprint" at the bottom of the page.

- 1099-NEC or 1099-MISC Forms: For questions regarding a 1099-NEC or 1099-MISC Form that you personally received or need to obtain from the University, please contact the University Financial Helpline at 612-624-1617 or [email protected].

- 1099-R Forms: For questions regarding a 1099-R Form which is used to report the distribution of retirement benefits such as pensions, annuities or other retirement plans that you received or need to obtain from the University, please contact the Office of Human Resources at 612-624-8647.

- 1098-T Forms, Statements of Tuition, are handled by One Stop Student Services. They have developed a very informative FAQ list which is hosted on our site. If after consulting the FAQ on 1098-T forms you still have questions, please consult your campus One Stop directly:

- Twin Cities 612-624-1111 or 1-800-400-8636, [email protected], onestop.umn.edu

- Crookston Business Office: 218-281-8331, [email protected]

- Duluth 218-726-8000, [email protected], d.umn.edu/onestop/

- Morris 320-589-6046 or 1-800-992-8863, [email protected], onestop.morris.umn.edu/

- Rochester 507-258-8069, [email protected], onestop.r.umn.edu/

Payments to International Visitors

Departments sometimes provide monetary support to individuals from countries other than the U.S. when the individuals are visiting the University of Minnesota. For information about tax treatment and withholding, see the memo on payments made to visitors from non-U.S. countries.

Tax Management Office Guidelines

Job Aids

Payments to Students Resources

Departments often need to make various types of payments to students. The resources below can help with determining what type of payment is appropriate for your specific situation.

It is important to make the correct type of payment so the University is compliant with IRS reporting requirements and financial aid limitations.

For assistance with deciding how to make a student payment, send details of the situation to [email protected].

Tax Management Office Guideline

Regents Tuition Benefit Program — Job-Related Graduate Course Exclusion Application

Regents Tuition Benefit Program - Exclusion of Education Benefits as Working Condition Fringe

Employees using the Regents Tuition Benefit Program may want to consider whether an income tax exclusion applies to the value of the benefit in excess of $5,250. When courses relate to current job duties, the value may be excluded from the employee’s gross income if the course qualifies as a working condition fringe benefit. See the Job-Related Graduate Course Exclusion Application.

For more information, see Tax Implications of Regents Tuition Benefit Program, appendix to the policy Regents Tuition Benefit Program.

In accordance with IRS regulations, the University Tax Management Office does not provide personal tax advice. To determine your eligibility for a higher education tax credit, a student loan interest deduction or a deduction for qualified education expenses, please contact a personal tax advisor or the IRS.

Tax-Exempt Debt

The University issues debt to fund various capital projects, including land and building purchases. The issuance process and post-issuance compliance are the responsibility of Debt Management. The University Tax Management Office works with the Debt Manager and several other departments on campus to manage the tax aspects of a tax-exempt debt issuance. As needed, the Tax Management Office will perform reviews of private use and arbitrage rebate relating to tax-exempt debt issuances.

The University has debt management guidelines that ensure each debt transaction conforms with all laws and regulations. Capital Project Management provides a portfolio of projects in design, projects in construction, and completed projects.

Private Business Use Working Tips

- Private business use (PBU) must be tracked by the TMO on an annual basis.

- PBU occurs when an outside non-governmental entity uses the TE funded space.

- The following activities will need to be analyzed by the TMO to determine if private use exists:

- Rental of debt-financed space to outside third parties

- Naming rights for non-individuals

- Research agreements with outside organizations

- Collaboration agreements with third parties

- Management contract

PBU Maps

The TMO has prepared maps of each of the campuses identifying the capacity for private business use within each building. Departments should refer to them prior to entering into any private business use arrangements. The following is information to help interpret the color coding (key) used in the maps.

- Buildings shaded blue do not have any TE debt on them and have no limits at this time for private use.

- Buildings shaded orange also have no TE debt and have capacity for additional private uses but HEAPR funds should not be used for any building improvements without first working with the TMO.

- Buildings shaded green have TE debt but have capacity for additional private uses.

- Buildings shaded yellow have TE debt and the TMO should be contacted prior to entering any additional private use agreements.

- Buildings shaded red have TE debt and the TMO should be contacted prior to entering any additional private use agreements. In addition, HEAPR funds should not be used for any building improvements without first working with the TMO.

- Buildings shaded gray have not yet been analyzed by TMO. Departments should contact TMO before entering into any private business use arrangements or before requesting HEAPR funds to be used for building improvements.

Minneapolis PBU St. Paul PBU Morris/Crookston PBU PBU Duluth PB

Tax Management Office Guidelines Applicable to Tax-Exempt Debt

- TMOG #1 - University Tax-Exempt Bonds and Private Use Guidelines

- TMOG #4 - Research and Private Business Use

- TMOG #9 - Fifty Day Rule

- TMOG #10 - Qualified Improvement Exception

- TMOG #12 - Tax-Exempt Bond Expenditure Allocation Rules

- TMOG #13 - Arbitrage Rebate Compliance

- TMOG #14 - Private Business Use

- TMOG #15 - Form Series 8038 and Capital Leases

Tax-Exempt Status

The University's Exempt Status

The Internal Revenue Service has ruled, at the request of the University, that the Regents of the University of Minnesota (University) is an “integral part” of the State of Minnesota for federal tax purposes. As such, the University is exempt from federal income tax, except the tax on unrelated business income.

The Tax Management Office has several helpful resources for explaining and substantiating the University's tax status:

- Memo from the Tax Director

- Letter from the IRS - copy of a letter from the IRS confirming our tax status

- LTR 147C - Frequently we are asked to provide a letter from the IRS verifying our name and EIN (Employer Identification Number)

Since the University is an "integral part" of the State of Minnesota, we do not have a Form 990 filing requirement.

Form 6166 - Certification of U.S. Tax Residency

Form 6166 is a letter certifying that the University is a resident of the United States for purposes of the income tax laws of the United States. University units may use this form to claim income tax treaty benefits and certain other tax benefits in foreign countries.

If you need a Form 6166, please request one by emailing the University Tax Management Office at [email protected]. The Tax Management Office has Form 6166 for each country in which we have an income tax treaty. So that the Tax Management Office can monitor their use, blanket requests for multiple forms will not be fulfilled.

The form may be different depending on the country, so we do need specific information when units request forms. When requesting Form 6166, please provide the following information to [email protected]:

- Unit name and a description of the University activity for which the Form 6166 is requested

- Foreign country or countries of the activity

- Date or year of the activity

- University address to send the form(s)

Please note, we cannot email Form 6166 because it is printed on U.S. Department of Treasury stationery and voided when scanned. Because official University mail handling must occur at University locations, the Tax Management Office will only send Form 6166 to University departmental addresses using intercampus mail. Units will be responsible for mailing it to their external contact from a University location.

Unrelated Business Income Tax (UBIT)

The University of Minnesota is exempt from federal and state income tax as an integral part of the State of Minnesota, however, revenue-generating activities not directly related to the University of Minnesota’s exempt purposes of research and discovery, teaching and learning, and outreach and public service may be subject to federal unrelated business income tax (UBIT). Congress imposed UBIT on exempt organizations to eliminate a source of unfair competition by placing tax-exempt organizations on the same basis as nonexempt organizations with which they compete. When a revenue-generating activity is a trade or business, regularly carried on, that is not related to the University’s mission, it may result in UBIT.

Internal Revenue Service Regulations go into great detail in defining these concepts. For UBIT purposes, trade or business generally means any activity that is carried on for the production of income from the sale of goods or the performance of services. We consider whether the University intends to make a profit from an activity when determining whether it is a trade or business. The frequency and continuity of the activity and the manner in which it is pursued are considered in determining whether it is regularly carried on. Often the most difficult determination is whether the activity is related to the University’s exempt mission.

Numerous Private Letter Rulings have been issued by the IRS providing guidance on when an activity is unrelated to a particular exempt purpose. There are also numerous statutory exceptions for particular activities and exclusions for certain income.

New activities that go through the external sales application process are reviewed by the Tax Management Office to determine whether the activities are included in the University’s UBIT reporting. UBIT determinations are very dependent on the facts and circumstances of each activity.

UBI Working Tips

- Activities with University departments are not UBI.

- University sponsored activities are not UBI.

- Agreements with external taxable entities may result in UBI and all agreements should be reviewed by the Tax Management Office.

- Third party catering/cafe agreements may result in UBI and all agreements should be reviewed by the Tax Management Office at the time the contract is being developed.

- Unrelated Business Income Tax Procedures, and Collecting and Remitting Minnesota Sales Tax on External Sales Transactions

Tax Management Office Guidelines

Contact Us

Campus Mail: Code 2715A

Phone: 612-624-1053 | Email: [email protected]

University Tax Management

2221 University Ave SE, Suite 100 Minneapolis, MN 55414